Retirement planning

Retirement planning

It's never too early to plan ahead and understand your options within the Swiss pension system.

Retirement planning

It’s never too early to start thinking about your financial needs for retirement. This means making sure you understand how the pension system in Switzerland works.

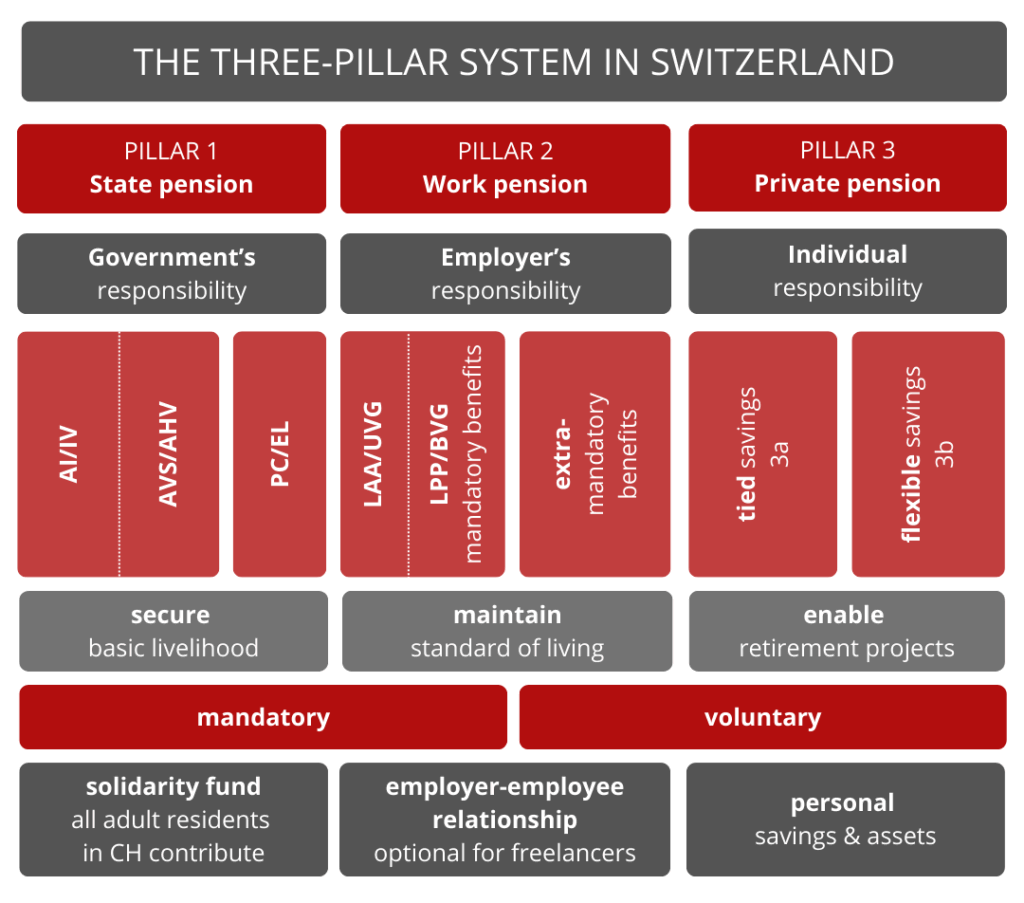

On retirement, you will begin to receive payments based on the financial contributions that you have made into the pension system. In Switzerland, this system is divided into three sections, which are called ‘pillars’.

First pillar

The first pillar is the state-controlled pension. Payment into it is compulsory for everyone living and working in Switzerland, and its purpose is to cover your basic needs in retirement.

The amount you receive will depend on:

- The number of years you have been contributing to the pillar

- Your salary level

- Whether you have missed payments for a period of time

- Whether or not you choose to retire before or after the official retirement age

Second pillar

The second pillar is compulsory for employees earning over a certain threshold (the amount of which usually increases slightly every two years), and payment into the pillar is shared with your employer. Those who are self-employed or who earn under the threshold can voluntarily choose to contribute through a provider of their choice.

This pillar is designed to help you maintain your standard of living. On retirement, the amount in your second pillar is added to the first.

If you are leaving Switzerland before the legal retirement age, depending on your destination, you may be faced with a choice about your occupational pension. We can help with investment plans so that your money keeps earning, even if you are between jobs.

Third pillar

For many people, the combined benefits from pillars one and two are unlikely to be sufficient to maintain a preferred standard of living. The majority of residents, therefore, opt to contribute to a third pillar.

The third pillar is your personal private pension plan. Contributions are voluntary but it is strongly recommended. This pillar can help make up for any gaps or shortfalls in your contributions to the first and second pillars, and it can also offer increased death and/or disability benefits.

There are two ways a third pillar policy can be taken out: 3a and 3b.

3a third pillar:

- It is tied to your retirement age and is tax efficient.

- Contributions can be deducted from your taxes each year up to a maximum amount fixed by the government. For example, these amounts are CHF7056 for employees and CHF35,280 for the self-employed (capped at 20% of net income) in 2024 (respectively CHF7258 and CHF36,288 in 2025).

- In addition to the tax benefit, any earnings from accrued interest are exempt from taxes for the duration of the policy.

- On retirement, the lump sum benefit is taxed at a preferential rate.

- Capital paid into a third pillar pension is a popular way of financing residential property, as the capital can be used to finance a home.

- It is possible to contribute to a third pillar via a bank or insurance company. Your choice will depend on your personal circumstances.

A 3b pillar consists of savings in the form of cash, savings accounts, investments, and life insurance. There are no restrictions on this pillar in terms of length of contract or maximum contributions.